Core and Satellite Portfolios: A Structured Framework for HNI Wealth Creation

April-2026

12:00 PM

At the start of every financial year, something subtle changes. Investors begin to think differently, act differently and, in many cases, take decisions they had been postponing for months. This shift in investor behaviour financial year patterns is not random. It follows a predictable psychological cycle.

For high-net-worth individuals and ultra-high-net-worth individuals, this behavioural shift can either improve decision-making or introduce unnecessary noise. The difference lies in whether the shift is guided by structure or driven by emotion.

Understanding investor behaviour financial year trends is not about predicting markets. It is about understanding how decisions are made, especially when the calendar resets.

A new financial year creates a natural reset. It feels like a clean slate.

This reset influences investor behaviour financial year patterns in a meaningful way:

While this can be useful, it can also lead to decisions that are not aligned with long-term wealth goals.

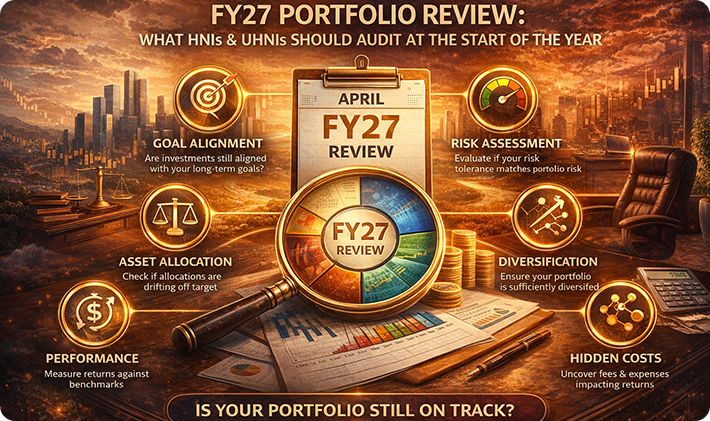

Over time, portfolios become complex. Multiple investments, fragmented tracking and lack of structured reviews reduce clarity.

At the start of FY27, this changes.

This shift in HNI and UHNI investment behaviour is driven by:

This aligns with financial year planning for HNIs and UHNIs, where clarity leads to better outcomes.

One of the strongest drivers of investor behaviour financial year decisions is recency bias.

Investors often base decisions on recent performance rather than long-term consistency.

This leads to:

These are among the most common behavioural biases in investing, especially visible among HNIs and UHNIs managing larger portfolios.

At the start of the financial year, there is a natural tendency to act.

For HNIs and UHNIs, this can translate into:

These emotional investing mistakes often reduce long-term efficiency rather than improving it.

A structured approach to financial year planning for HNIs and UHNIs helps reduce behavioural errors.

Instead of reacting to markets, decisions follow a defined process:

This improves investment discipline strategy and ensures decisions remain objective-driven.

Investor behaviour becomes more stable when the portfolio itself is structured clearly.

For HNIs and UHNIs:

Similarly, understanding tax saving vs tax harvesting strategies helps avoid decisions driven by short-term considerations.

Trying to fix everything at once creates unnecessary complexity.

Recent performance does not indicate consistency.

Lack of structure leads to repeated inefficiencies.

These patterns are common in wealth decision behaviour for HNIs and UHNIs and often reduce long-term outcomes.

Markets are unpredictable. Behaviour is controllable.

Our analysis shows:

This makes managing investor behaviour financial year patterns critical for both HNIs and UHNIs.

The beginning of FY27 should be used to:

For HNIs and UHNIs, this improves long-term wealth behaviour and ensures decisions remain aligned with objectives.

Every financial year brings a new opportunity, not just in markets, but in behaviour.

For HNIs and UHNIs, understanding investor behaviour financial year patterns allows decisions to become more structured, more disciplined and more aligned with long-term goals.

We believe wealth creation should be uncomplicated. When behaviour is aligned with a clear process, outcomes become more predictable and more consistent.